I'm

still trying to get my head around the concept of the blockchain and other 'distributed ledger' technologies, how they are useful and what else needs to happen to harness their potential. To that end, I'm trying to ignore the 'virtual currency' use-case that seems to get everyone tied up in knots. I mean, the Internet is more than a money remittance platform, right? Well, the concept of a 'distributed ledger' is similarly broad - maybe broader than the Internet. According to

Ethereum, "a platform for decentralised applications",

even the word 'ledger' is too limiting.

Recently, I read the '

call for evidence' on this topic from European Securities and Markets Authority (ESMA), especially as there's been a lot of talk about using the blockchain to cut the time and cost of central clearing and settlement in the financial markets.

Yet, as the call for evidence itself shows, even ESMA is struggling to understand the uses beyond investment products which (a) provide exposure to a virtual currency without buying it, or (b) require you to actually trade in virtual currency in ways that are recorded in the relevant 'blockchain' or other currency ledger.

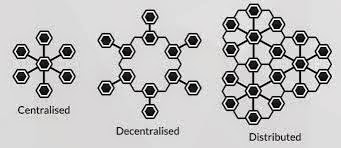

This could be because ESMA is viewing the technology through the lens of the existing, heavily intermediated financial market structures and how these might be somehow replicated using the new technology (see the two diagrams in section 4). But as I've complained for years, financial regulation (for which ESMA is partially responsible) funnels investment funds and opportunities into marketplaces where comparatively few intermediaries are allowed to operate - so they can charge what they like and not bother innovating, except to suit themselves (high frequency trading?). Internet technology has helped a bit, by making it cheaper to build and host systems etc, but that technology is still based on the idea that transactions occur in separate computers and the related data remains locked away in proprietary databases, or displayed only to subscribers.

Distributed ledger technology seems to herald something far more revolutionary.

As I see it, these technologies basically involve publishing machine-readable applications or programs that can be read by any device running the same technology. Each market participant just needs to publish or display to others what it is offering or what it needs and any 'deal' will be recorded or coded on a nominated blockchain or ledger. Certain stuff can still be kept secret, but enough information can be shared to enable the computers to record the deal publicly so that everyone knows the deal was done.

Take an ordinary consumer transaction like renting a car. The rental car company's computer could publish a certain program that identifies the company itself (pseudonymously), a specific car, the make/model, its current location and the price to rent it for the day (including full collision damage waiver!). If I need to rent a car, I could publish some code that identifies me (pseudonymously), what type of car I need, where, when, how much I'm prepared to pay per day, the payment method and how the rental company can authenticate my driver's licence. Our computers find each other, like what they see and submit a transaction to a third computer which writes it up in code that instructs other computers to take my payment, send me the collection details and so on. In other words, as well as being an open record that the transaction exists, the code can also refer others to more detailed information where necessary.

It seems that very little should need to change outside the above scenario for this begin to happen, since the programming languages are now expressive enough to enable such codes to be written about every day transactions without a lot of fuss over industry standards. However, over time the same technology could be at work all over the place in more technical scenarios. For instance, my driver's licence could also just be a computer code available on a separate blockchain or ledger, to which the rental company's computers could be referred to check when it expires, whether I have any demerit points and so on. Even credit references and so on might be ascertainable in this way.

In other words, all sorts of computer applications could run "on" the blockchain and/or act as gateways between/among blockchains and between blockchains and the applications running on the ordinary old Internet, like social media, email or those running on mobile networks, like SMS. So, in the example, a program running on the blockchain could initiate a text message telling me where and when to pick up my rental car.

.bmp)